Raise Millions

Highlights

So if you can get away with securing money through bootstrapping, crowdfunding, government programs, banks, or even alternative lending models like Paintbrush… we actually recommend not fundraising to keep 100% ownership of your company.

These investment rounds are typically small, ranging between $100k - $1M. The money will likely come from your family, friends, angel investors, and pre-seed funds like Hustle Fund (that’s us!). The goal at this stage is to get enough money to go full-time on your startup, build your product, and start generating some traction.

Learn from Eric’s mistake and incorporate your company in Delaware. Here’s why Delaware C-Corps are so advantageous.

There are lawyers and possibly automated legal services that can help you switch over to a Delaware C-Corp. So if you’re running a venture-backed business, switch to a Delaware C-Corp and keep more money upon your exit.

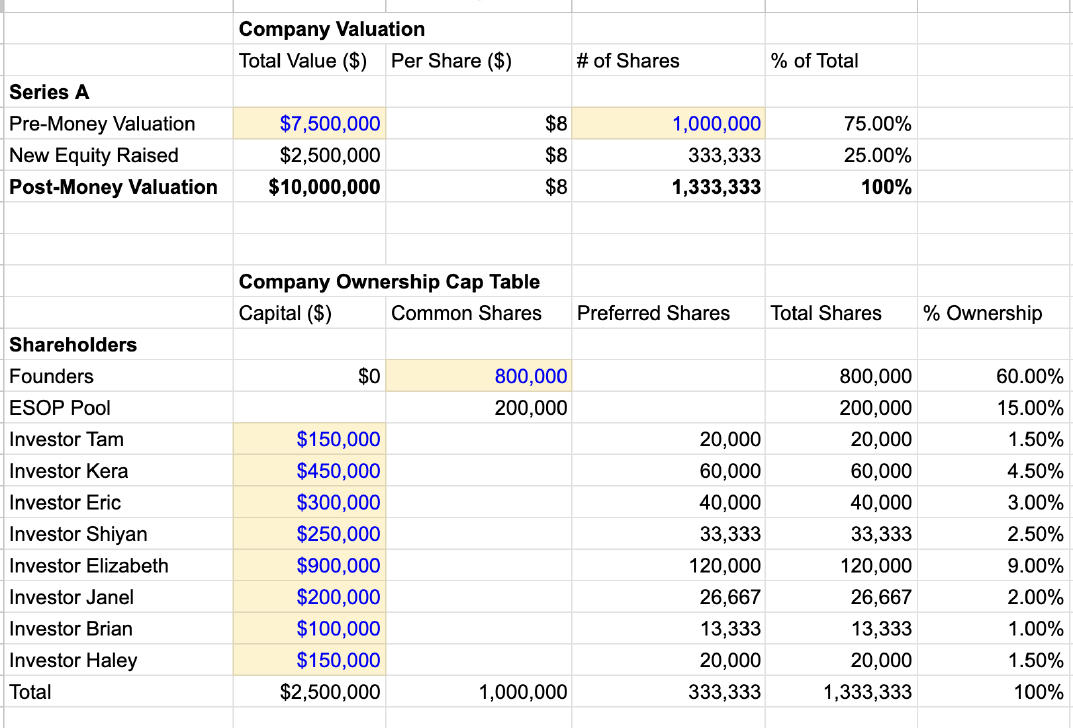

The gold standard is for the founders to still own the majority (more than 50%) of the pizza after their Series A round. It’s common to lose the majority by the time you raise your Series B. But as I mentioned earlier, this shouldn’t bother you if the value of the pie is high enough.

In non-pizza terms, a SAFE isn’t equity you sell to your investors, rather it’s the promise of equity in the future. Think of SAFEs almost like an IOU; you’re not issuing any equity yet… but once you have an equity financing round, an acquisition, or an IPO, that SAFE will get converted into equity. If your startup crashes and burns, the SAFEs are worthless.

If you use pre-money SAFEs, learn how to calculate and keep track of how much pizza you’ve sold. Instead, use post-money SAFEs to have clarity… and sleep well at night knowing you still have enough pizza in the fridge to enjoy later.

While the other factors do matter, a startup’s valuation is not actually about how much your company is worth, but about the supply and investor demand of your round.

In practical terms, determining your valuation is less about your “actual” worth and more about what investors are willing to pay. So founders can set a value for their own startups, but VCs will also perform due diligence to determine a valuation they’d feel comfortable investing at. The two sides may then negotiate an acceptable valuation for both parties.

Decreasing the valuation is a signal to investors that there is something wrong with the business. And since investors see anywhere from 10 to 1000 pitches every month, they’re more likely to invest their money in a new company instead of writing this founder another check.

joining a team with a high valuation means that the price for the stock options is also high. Employees will realize that they can’t actually afford to buy their options.

The savvy people who are smart enough to ask about valuation and exercise price will realize that the opportunity isn’t as good as they thought. So if you have too high of a valuation, hiring those people will become very difficult.

Founders get common shares while investors earn preferred shares. There are three main differences.

• Voting power: Common shareholders get to vote on important company decisions whereas preferred shareholders usually don’t have voting rights.

• Dividends: Preferred shareholders get preference on liquidity when the company IPOs/exits. This means they get paid out before the common shareholders.

• Risk: Common shares are a bit riskier. If the company has to close down, founders will be the last to get any money back from what’s left, whereas preferred shareholders may recoup some of their money.

We recommend founders use Pulley (a plug for one of our portfolio companies), which makes cap tables super easy to understand even if someone invested through SAFEs.

Investors typically expect founders to set aside 10% of the pie for ESOP but this percentage amount can be negotiated. 15 years ago, this percentage was typically 15-20%, and we may revert back to that if the markets get worse.

A rough rule of thumb is that founders should aim to double their valuation every round.

What is the minimum requirement to keep the company running? How can you reduce your burn rate? How can you cut expenses? Are there creative ways to generate revenue in the interim?

August is the absolute worst time to raise money. VCs basically take the entire month off for summer vacation.

five most essential parts for a great pitch.

- team

- problem

- solution

- market

- traction

When you’re pitching your team to an investor, consider how you can convince her that your team is uniquely positioned to solve this problem.

The book The Founder Dilemma cites that 6 out of 10 startups fail because of co-founder conflict. That’s why it’s so important for investors to feel confident in the co-founder relationship. They want to know that co-founders can make decisions together, communicate openly, share the burden of work, and disagree without tearing the company apart.

when you’re pitching the “team” portion of your company to an investor, show that you and your co-founder are a good fit.

Every unicorn business:

- solves a real problem…

- … that’s important enough for people to pay to fix

- … and applies to a large audience

If your problem slide doesn’t quickly demonstrate those three points, investors might not even look at the rest of the deck. So this slide is super important.

Your problem slide should give efficient and compelling responses to these three questions:

• What is the problem?

• How do you know it’s a problem?

• Who needs a solution to this problem?

Inaccurate statements raise red flags for investors. It makes us think that you either aren’t honest or you haven’t done your research.

Investors want to see that you’ve done your homework. Share how you arrived at your problem statement. Include data that you’ve gathered from your customer research. Get specific by using real numbers that matter. This will better convince investors that what you’re working on is a massive problem.

There are 3 important things to consider when putting together your “solution” slide:

- Differentiation

- Framing your story

- Product vision

focusing on the most differentiated component of my business

When you explain your solution, don’t focus on what you have right now. Instead, sell them on your product vision.

Do we believe that you are a founder with the right team and market to support a 100x outcome?

If you’re looking to raise money from a venture fund, make sure your market can be measured in billions of dollars. This shows VCs that there is room to grow and capture a slice of the huge market. If your market is smaller than that, consider raising from angel investors. During those conversations, ask what success looks like to them to see if your goals fit with their vision.

For early startups, you don’t have many resources. So it’s really important to go after a specific niche. The more targeted and specific the niche, the better it’ll be. At the same time, you need to have some vision of expansion because investors want to understand how this can become a big opportunity (like Hubspot).

The best way to display this in a pitch deck is through three circles that describe your different markets. For Hubspot, it can look something like

- Small market: SMB SEO tool

- Medium market: SMB marketing automation

- Large market: Enterprise marketing automation

This shows investors the initial market you’re in now and what your growth plan may look like in the future.

if you’re super early stage, show investors something – an MVP, results from your small experiments, or even a Figma design – will go a long way.

For an early-stage company, the pitch deck has one purpose: to drive enough interest in your business to schedule a meeting. That’s it. It should not (and will not) convince someone to invest in the company.

You should be able to accomplish that goal in 5-10 slides, max. If your pitch deck is 12+ pages, you are likely providing too much information. Too much information can be risky because it gives investors more opportunities to find red flags.

Here’s the solution: omit unnecessary details so that investors can focus on the details that matter most.

Your most powerful elements will get lost in all the noise. Instead, cut anything that isn’t absolutely necessary. For example:

• That slide about how many people you’re going to hire → Focus instead on the amazing team you already have (even if it’s just you)

• Those inspirational quotes by Benjamin Franklin → Cut ‘em. You’re innovating. We get it.

• Screenshots of the product → These won’t be nearly as powerful as a live demo of your product.

• Your revenue projections for the next 5 years → Tell us instead what about your growth over the last few months.

If you’re having trouble ruthlessly editing your own work, try presenting your deck to someone who knows nothing about your industry. Like a parent, grandparent, or sibling.

As you explain your business to someone who doesn’t understand your industry, you’ll quickly realize what is (and what is NOT) a powerful addition to the deck.

On AngelList, you can find investors who have previously invested in startups similar to yours.

Our recommendations:

• Include one line about your business

• Use a few bullet points to indicate the value proposition, current pilots, and/or traction

• End with a clear call to action, like “Do you have time for a 15-minute call on Wednesday to talk about fundraising?”

Here’s our advice: Change the way you ask. “Can you think of one person who might be interested in hearing about my company?”

This new question is wildly more effective. Most people can think of one name with ease. The hurdle is far lower and the ask is achievable. Oftentimes, that person is the richest person they know.

Here are a few common flags that often prevent us from taking a meeting:

• If the founder isn’t working on the business full-time

• If the revenue model is based entirely on ads

• If the team seems distracted with many different opportunities, rather than focused on the core business

• If we’ve already invested in a similar company

• If the company requires a huge amount of capital to be raised before you can take the MVP to market

• If the valuation is super high

Basic elements of an elevator pitch

- Keep it short. Aim for 30-60 seconds.

- Be straight to the point. Highlight 2-3 impressive things about your company, nothing more.

- End with a specific call to action. Ask “Would you like to learn more?” to investors if you’re looking to fundraise. Or ask “Do you have any feedback?” to founders if you’re looking to improve your pitch.

The goal of an elevator pitch is to leave the investor curious to learn more about your startup. It’s inappropriate to ask, “Are you ready to put $100k into this idea?” right after a pitch.

Eric shows his real background because it shows what his life actually looks like. Vulnerability is often reciprocated and that’s where you can both start to form a more personal connection.

Zoom tip: Set your camera to be at eye level to make the meeting feel more conversational.

totally ok to not use a slide deck during your first meeting.

When you use a slide deck, you automatically enter “presenter mode”, which gives the meeting a clear power dynamic. Both parties become uncomfortably aware that one of you is the decision maker (hint: it’s not you).

When you have a relaxed conversation with someone, the power dynamic feels more balanced. And when the dynamic is balanced, you can connect more deeply as humans. By the way, you can still pitch yourself and your company without using a pitch deck.

After the initial small talk, ask the investor to tell you a bit about themselves:

• How they got into venture

• What their role at their firm is

• A deal the fund recently completed

After they share their story, you can tailor your pitch to the VC’s context.

As you share more about your similarities, notice their reactions on Zoom. If the other person is looking away or fading off, change the subject to what they care about. If they’re nodding and smiling, those are cues to lean more into your story.

A red flag for most investors is when founders get SUPER defensive, or even dismissive of the questions or ideas that investors bring to the table. This is because a defensive founder indicates that they are probably not coachable.

Our team at Hustle Fund looks for founders with growth mindsets. People who are open to receiving new information and hearing new perspectives, then changing their worldview based on that new information. It’s a big red flag when it appears the founder lacks that mindset.

If you find that investors are grilling you on your business, that’s actually a good sign. This means the investor is interested in the business and wants to dig in more.

the actual numbers meant far less to us than the founder’s understanding of those numbers. Because without that knowledge, how can the founder know where to focus his time and resources? How will he know what’s driving the business, and what changes should be made to improve it?

Prepare as much as you can to answer these questions. Respond gracefully and honestly. You’ll be on the right path.

Before taking an investor meeting (or even reaching out), do your homework and research investors. Make sure to reach out to investors who are actually a good fit for your business (stage, sector, amount, what they look for, etc). Most websites will spell his all out – especially newer micro funds who are trying to differentiate themselves in the market by going after a specific niche.

here’s a list of questions you should ask investors when you meet them:

• How big is your fund? (for VCs)

• Where are you in your fund? (for VCs)

• When will you need to fundraise again? (for VCs)

• Do you lead rounds? (for VCs)

• What is your typical check size?

• Do you reserve capital for follow-on?

You should find out an investor’s cadence:

• How many seed deals have you done in the last 6 months?

• How many seed deals do you anticipate doing in the next 6 months?

• How long does your process typically take?

And how decisions are made:

• What is involved in your process?

• Who is the decision maker? (for VCs, although sometimes angels need to consult their families or friends)

By the end of the meeting, you should understand:

• Everything about an investor’s decision-making process

• Whether you have a champion to take this to the decision makers (whether it be partners at a firm or their family)

• What the concerns are with your business in their eyes

• What the CONCRETE next steps are

it’s good to set expectations before you hang up, saying something like “I’ll follow up in the afternoon” or “I’ll get back to you within 24 hours.” And then actually follow up within the timeline you’ve set.

A great fundraising process is only 20% about pitching. The other 80% is all about organization.

If someone isn’t returning your messages, you should ping them at least 10 times before marking them as “ghosted.”

If people have committed, we recommend being aggressive and following up every two or three days. This shows that you’re committed to making this work and are certain you have given them all the materials they need to make a decision.

For the people who have rejected or ghosted you, you should keep reaching out. One time Eric reached out to an investor 12 times with no response. Then, on the 13th attempt, that investor replied. He ended up committing half a million dollars into Hustle Fund.

So a rejection is never truly a rejection until you get a hard “no.”

Whether they committed capital or turned down the opportunity to invest, invite all the investors you connect with to join your investor newsletter.

This is a monthly update on what’s happening in your startup. This newsletter has two benefits:

- It keeps your existing investors engaged – and helps you make important asks when you need support.

- It’s a crazy effective fundraising tool – the people who said “no” to you are looped into your progress and may convert into investors down the line.

It’s possible to train people to read a specific section of your newsletter by giving them a chance to see their own name listed. In our Hustle Fund investor newsletter, we give a dozen shout-outs to people who have helped us in the previous month. People often read to the end to see if they’re listed.

This is also a subtle name-dropping element. Including the people who have helped you gives everyone a sense of the community you’re surrounding yourself with. This can also potentially FOMO people into helping you, as well.

Consistency is paramount. Whether it’s once a month or once a quarter – we recommend once a month – you want the folks on your investor newsletter to get used to hearing from you at a regular cadence. It’s a great way to build trust with your investors. They’ll see you as reliable and trustworthy, and will be more likely to recommend you to other investors and strategic partners in the future.

If you ask for generic feedback, there may be too much “analysis paralysis,” and it’s going to be hard to get an answer. But when you ask for just one reason or one thing that you could improve, this makes it easier for the person to respond.

Ask targeted and action-oriented questions like, “What is one thing you think that I should change about my pitch?” You can even gather a few founders into a small mastermind group to do this activity together. Each person pitches and the other people in the group give feedback for 10-15 minutes. This allows you all to gather input from multiple perspectives and learn from each other.

An investor’s assistant is actually the most powerful person at the firm. They control the investor’s calendar, and while the investor may not 100% follow that calendar, the assistant may be able to nudge the investor or slot you in for another meeting if you’re still having trouble.

He could have avoided the drama if he didn’t skip a critical part of the fundraising process – conducting investor reference calls.

Investor reference calls are phone calls with other founders who have worked with your prospective investor. These reference calls usually take 10 minutes and will probably tell you everything you need to know. Trust us, putting in the time to complete this step will help you avoid toxic investors and save you years of pain.

When you accept money from a VC, there’s a checklist of things that they need to verify before they’re legally allowed to wire money to you. Things like:

• Certificate of incorporation

• Bylaws

• Board consents

• Founder stock purchase agreements

• Option plans

• 409a valuations

• Cap tables

And more documents. This can get more complex as you raise larger amounts of money. We recommend working with an attorney to make sure everything goes smoothly.

Pro Rata Rights — this allows the VC to invest more capital into your company in future fundraises typically on a “proportional” basis (the right to reinvest the amount required to maintain the equivalent percentage of equity as before).

Most Favored Nation Rights (MFN) — this means if a different VC comes in later in the fundraising process and successfully negotiates a lower valuation than the previous investor(s), the previous investor(s) can re-set their valuation to the lower amount.

Hop on the phone and verify your routing and account number to make sure the money goes to the right place. Please do this.

A data room is where founders store their most important company documents, like:

• Incorporation documents

• Bylaws

• Cap table

Basically, data rooms show that your startup is a legit company with actual employees. Super early-stage startups don’t need a data room. But we’ve met great pre-seed and seed-stage startups that have a simple Dropbox or Google Drive folder with their key documents.

One of my favorite quotes is “How you do anything is how you do everything.” As such, we can expect that the way founders keep track of their documents is reflective of the way they run their companies.

Impressive companies have everything organized and easy to find

• All documents are filed in the correct folders

• All important documents are included

• Everything is clearly labeled and easily searchable

Hustle Fund’s Document Requirements

We need fully executed and dated copies of the following:

• Action of Sole Incorporator

• Certificate of Incorporation

• Bylaws

• Board Consents/Minutes

• Founder Stock Purchase Agreements

• Option Plan and Stock Option Agreements (if any)

• 409A Valuation Report (if any)

• Capitalization Table (if any)

• Proprietary Information and Investments Assignment Agreements (PIIAs)

Some of these items like a 409A doc or cap table may be overkill, but the fundamentals are there. Any startup lawyer can easily provide this to a company.